Can A Reverse Mortgage Help You In Retirement?

Did you know around a quarter of the US population will be over 60 by 2060? Around 80% of older adults own their home. That helps reduce their living expenses while on a fixed income and acts as a source of equity.

But not everyone has enough saved for their retirement, leaving them looking for easy sources of extra cash. The conversation around reverse mortgages will likely increase in the coming years, since nine out of 10 baby boomers want to remain in their homes as they age. In 2022, over 64,000 homeowners tapped into this equity through a reverse mortgage.

Reverse mortgages can be useful financial resources, but they are complex financial products with long-term implications. Homeowning retirees must weigh the benefits against the risks before utilizing one.

How a Reverse Mortgage Works

In a reverse mortgage, homeowners borrow against the equity in their home, much like a home equity loan. However, traditional home equity loans expect regular monthly repayment. Reverse mortgage lenders have no immediate expectation of repayment. Instead, repayment is due once the homeowner sells the home, ceases to live in it as a primary residence, or passes away. The loan balance increases over time as interest accrues.

Depending on the mortgage terms, homeowners can receive the loan as a lump sum, monthly payments, or a line of credit.

Homeowners over 62 with no or little mortgage debt may qualify for this mortgage product. The funds help retirees supplement their fixed income and meet their financial obligations.

Reverse Mortgage Options

Three loan products are available under the reverse mortgage umbrella.

Home Equity Conversion Mortgages (HECMs) are the most applied for reverse mortgage product. These federally-insured loans can be used for any purpose and have no income requirements.

Single-purpose reverse mortgages have less expensive fees but can only be used for the purpose specified by the lender. State and local government agencies or local nonprofits are typical loan providers for this product. They offer them to help low-income seniors pay property taxes or fund home upgrades that keep aging residents in their homes.

Proprietary reverse mortgages are funded through private lenders for homes with a high value. They are not federally insured and involve a higher risk on the borrower, which also means higher interest rates.

Qualifying for a Reverse Mortgage

Applications for these loans peaked during the Great Recession, with over 100,000 HECMs issued each year from 2007-2009. However, applications have started to rise again and may continue to increase as America grows older.

If you’re thinking about a reverse mortgage, you’ll need to meet the following conditions:

- Must be 62 years or older

- Reside primarily in the property securing the loan

- Have a substantial amount of any existing mortgage paid off

- Capable of continuing payments for taxes, insurance, and upkeep

- Must receive HUD-approved counseling

- Approval from a lender and no outstanding federal debt

Benefits of Reverse Mortgages

Reverse mortgages do offer distinct advantages that can appeal to some retirees:

- Access to Equity: You convert part of your home’s equity into cash without selling your house. It’s a way to age in place while bolstering your nest egg. Funds with no use restrictions can pay for home renovations and medical bills or supplement the cost of daily essentials.

- No Monthly Payments: Unlike traditional loans, you’re not required to make monthly payments. The loan is typically repaid when you pass away, sell, or permanently move out of the home.

- Non-Taxable Funds: The money received is usually tax-free and typically does not impact Social Security or Medicare benefits.

Disadvantages of Reverse Mortgages

Do not overlook the potential downsides. They could have lasting consequences on your retirement, spouse, and inheritance plans.

- Diminished Equity: Over time, your home equity decreases as interest on the reverse mortgage increases. Any heirs must either pay the balance or will earn less from the probate sale. Also, consider your surviving spouse and if they will want to downsize. Any proceeds from a home sale must first pay off the reverse mortgage.

- Upfront Costs: Reverse mortgages can have high fees and other costs. That makes them an expensive way to borrow money compared to traditional home equity loans or lines of credit.

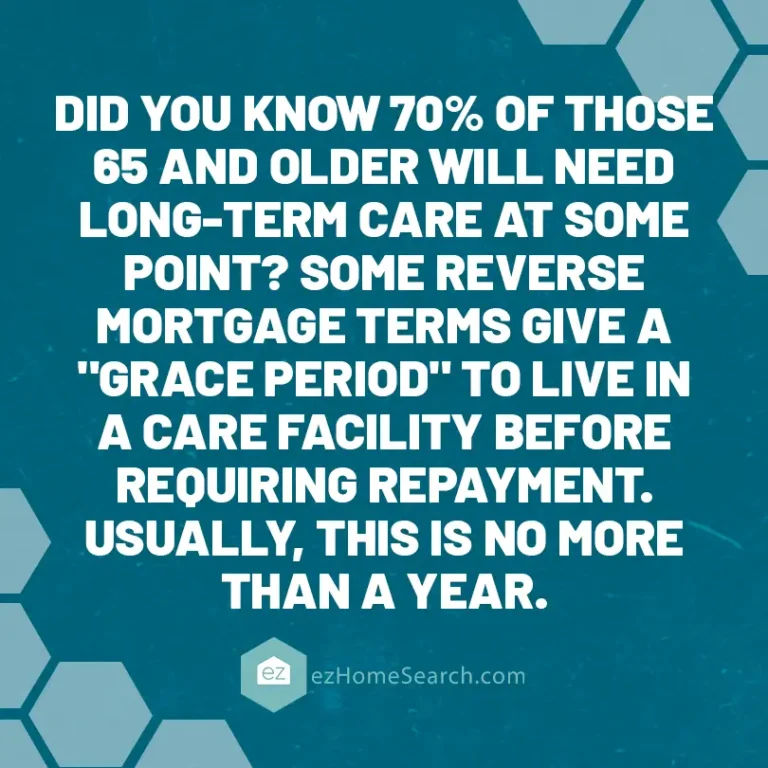

- Future Financial Options: Taking on the debt might limit your financial options later in life if you wish to move or need to pay for long-term care.

- No Coverage on Taxes and Insurance. The homeowner must keep the home in good condition, pay its property taxes, and make insurance payments. Those fees increase yearly, which can be a problem for fixed-income individuals.

- No interest deduction. The interest on the loan isn’t tax-deductible until the loan is paid back.

Things to Ask Before Applying

Before plunging into a reverse mortgage, protect yourself by answering a few pivotal questions:

- How does my financial situation look long-term?

- What are my retirement income goals and needs?

- Do I plan to stay in my home for many years?

- What are my heirs’ expectations concerning my estate and property?

- Will the surviving spouse be able to stay in the house?

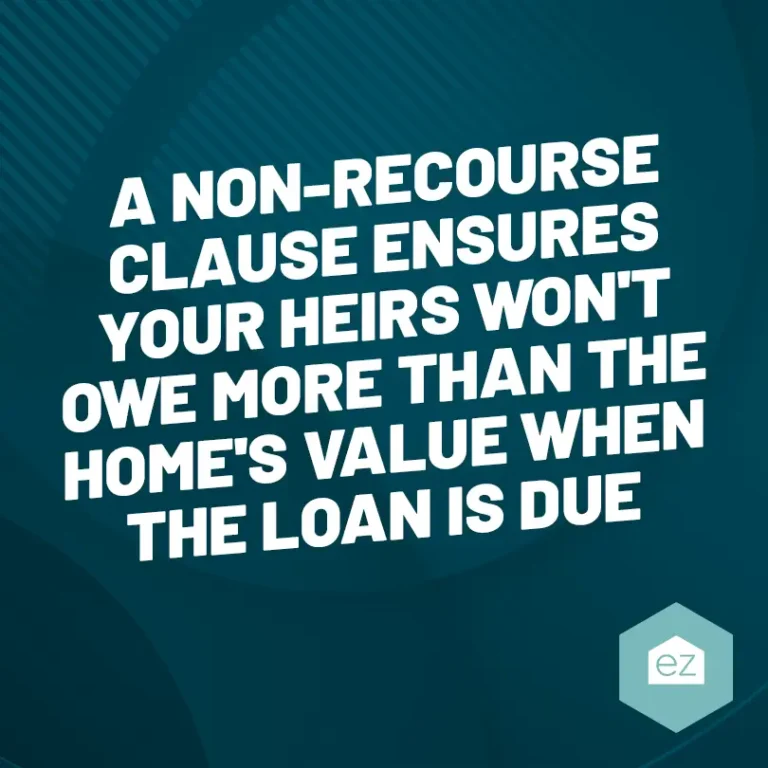

- Does it have a non-recourse clause?

- Will the loan have a fixed or variable rate?

- What are the upfront costs of the reverse mortgage?

Understanding your financial and personal situation will help you make an informed decision.

Reporting Reverse Mortgage Fraud

Be aware of the possibility of fraud in this area. Common schemes involve seniors facing foreclosure, needing home renovations, or equity theft. Report any suspected wrongdoing immediately to the Federal Trade Commission (FTC) or your state’s attorney general.

Final Considerations

Remember that a reverse mortgage is not a one-size-fits-all solution. It’s a commitment that profoundly affects your finances and estate. Seek advice from a financial planner or a trusted advisor who understands your situation. Additionally, reverse mortgage counseling is an invaluable resource to help you understand all the terms and conditions of a reverse mortgage loan.

Your ability to make informed choices can ensure you enjoy a secure and comfortable retirement, whether this includes a reverse mortgage or other financial strategies.

Start Your Home Search

Preston Guyton

Share this Post

Related Articles

Mortgage News

April 2024 Mortgage Market Update

Mortgage News

Mortgage Rate Update: Rates Increase In February 2024

Mortgage News

Mortgage Rate Update: Rates Stabilize In January 2024

Mortgage News