Conforming Loan Limits: A Guide for Homebuyers

Buying a house is a major life milestone. Besides finding the right one, navigating the maze of mortgage options available can be daunting. Add to that changing conforming loan limits, and it’s easy to see why someone can get lost.

Conforming loan limit is a term that crops up when prospective homebuyers learn about financing. Learn what that means and what makes a loan conforming. We break down who sets these limits and why they change. That way, you can make an informed decision about how to finance your home purchase.

2024 Conforming Loan Limits

For first mortgages in the continental US, Puerto Rico, and the District of Columbia, the limit is $766,550. High-value areas such as Alaska, Hawaii, and Guam are set at $1,149,825. However, some counties in the continental US may meet the higher limit. These conforming loan limits are reset each year.

Note that the forward mortgage limits and home equity conversion mortgage (HECM) limits are different.

What Is a Conforming Loan?

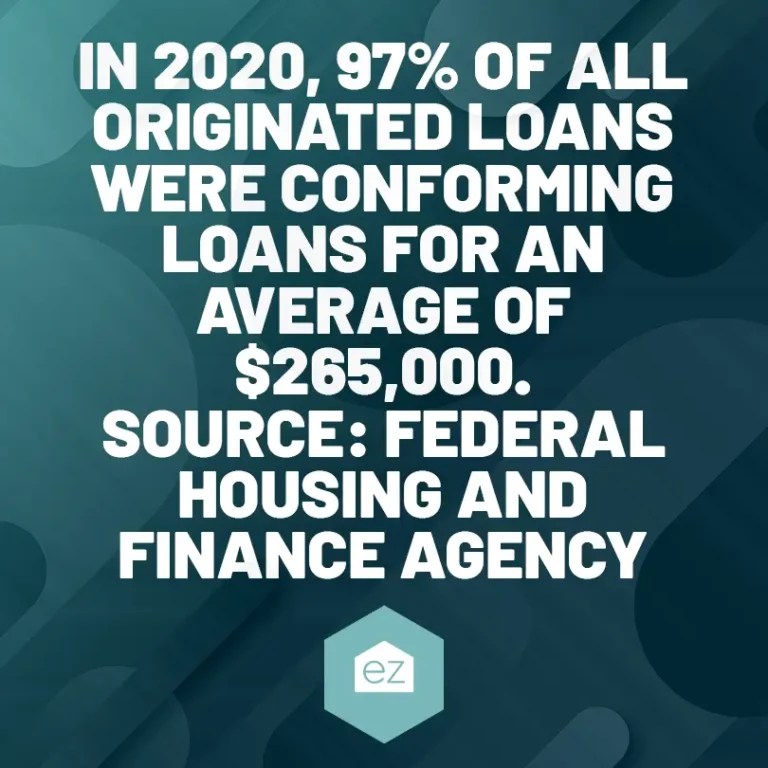

A conforming loan strictly adheres to the guidelines set by Fannie Mae and Freddie Mac. These guidelines set a maximum loan amount. Any loan over this amount is considered a nonconforming loan. Nonconforming loans typically have a higher interest rate because they can’t be guaranteed by GSEs, so lenders see them as high risk. Among these would be “jumbo loans,” hard money, or private loans.

Additionally, conforming loan borrowers must meet credit, income, and other financial requirements.

A conventional loan can be considered conforming or nonconforming. Among the nonconforming loans would be loans from the VA or USDA, where borrowers may not put down a payment. Or it could be a special program to help those with bankruptcy or foreclosures in the credit history.

What Are Conforming Loan Limits?

Conforming loan limits set the maximum loan amounts that Fannie Mae and Freddie Mac, government-sponsored enterprises (GSEs), are willing to buy or guarantee for conventional loans.

These limits are significant because they influence home loan terms and availability. Loans within these established limits are easier to sell on the secondary loan market. Lenders can package conforming loans together and sell them to investors. They offer more favorable mortgage rates on these loans because they know they can profit from selling a package to investors. Selling also helps them stay liquid so they can write more loans.

If you opt for a conforming loan, you may receive a notice a few months down the road that someone else now owns your loan. Chances are high that your mortgage originator will bundle and sell your mortgage. Behind the scenes, Freddie Mac and Fannie Mae purchased it and turned it into a mortgage-backed security.

Where Can You Find Conforming Loans?

Most banks, credit unions, and mortgage lenders across the United States provide conforming loans. Since Fannie Mae and Freddie Mac back them, lenders see these loans as having less risk. And, they are more willing to offer these loans with reasonable terms like lower down payments and competitive interest rates. The associated risk is reduced since they can sell the loans to the GSEs.

Why Do Conforming Loan Limits Change Annually?

Every year, US home prices change. It’s a combination of inflation, appreciation, and willingness to buy. For that reason, conforming loan limits adjust yearly to reflect average home price changes. The idea is to ensure that the average American buyer can still access affordable financing.

When home prices rise fast, the conforming loan limits may increase substantially to match the market conditions. Remember, the change is to facilitate continued access to affordable mortgages.

Who Changes the Limits?

The Federal Housing Finance Agency (FHFA) sets conforming loan limits each year following the permanent formula created under the Housing and Economic Recovery Act of 2008 (HERA).

The FHFA also oversees Fannie Mae and Freddie Mac, the two GSEs that back conforming loans. It uses their House Price Index (HPI) report and other data to assess real estate market price trends and adjust the loan limits.

Understanding Conforming Loans

A loan conforming to these limits may mean the difference between securing an affordable mortgage rate or taking out more expensive jumbo loans. Stay current with evolving loan limits and discuss with your mortgage advisor how they may affect your home purchase. After all, knowing the game’s rules lends an advantage when navigating the complex world of home financing.

Start Your Home Search

Preston Guyton

Share this Post

Related Articles

Buying a Home

What to Know About Termites In Your Home

Buying a Home

What to Know About Spray Foam Insulation

Buying a Home

5 Most Affordable Places to Buy a Home in Tennessee

Buying a Home